Family office convoys no longer pause in London or Singapore.

At first light in Lomé, a UAE patriarch initialed a term sheet for Togo’s largest solar park while customs agents off loaded turbine blades at the port. By lunch, US $150 million in Gulf capital was moving south. Moments like these capture a quiet—but fast accelerating—shift in South South finance that now places GCC family offices at the heart of Africa’s growth story.

1. Why Now? The Macro Tailwinds

Diversification Meets Demographics

Gulf sovereign road‑maps—from Abu Dhabi’s UAE‑Africa Gateway to Riyadh’s Vision 2030—all share one theme: non‑oil growth above 4 percent. Africa’s young population and demand for real assets offer a natural outlet.

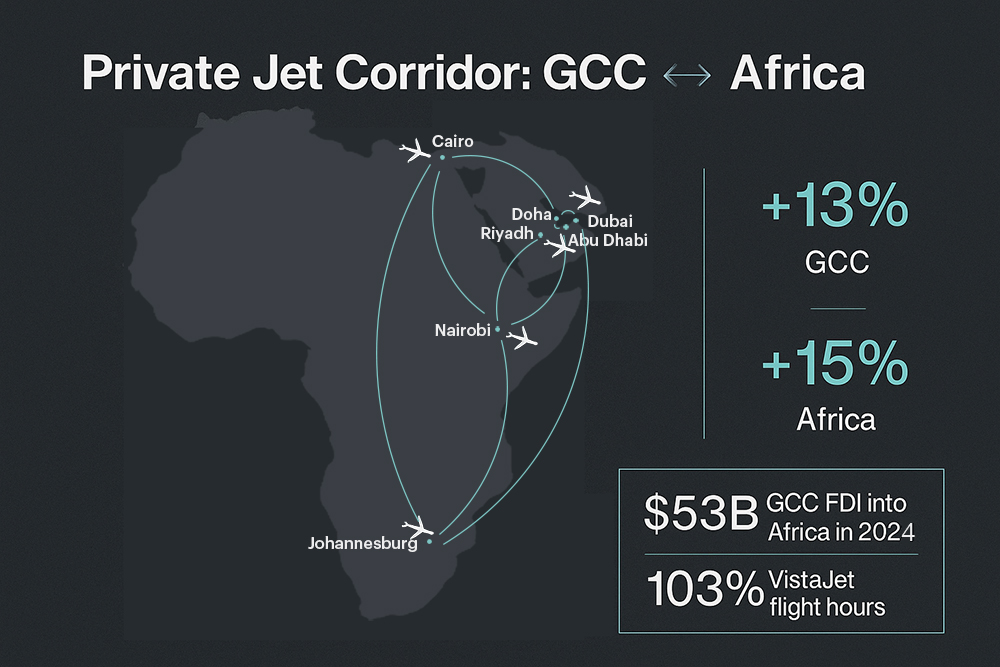

- Deal velocity: GCC firms announced 73 green‑field projects worth US $53 billion in 2024 alone.

- Long‑run momentum: Cumulative Gulf investment topped US $100 billion (2012‑22), led by the UAE (US $59.4 bn), Saudi Arabia (US $25.6 bn) and Qatar (US $7.2 bn).

Matching Capital to Continental Need

Africa’s infrastructure gap—US $130‑170 billion a year—shaves two points off GDP. Gulf balance sheets, flush with IPO and hydrocarbon cash, are hunting precisely these yield‑rich assets.

- AfCFTA tailwind: A borderless market of 1.7 billion consumers and US $6.7 trillion in spending by 2030 is coming online.

- China steps back: Beijing’s new lending fell from US $28.5 billion (2016) to < US $1 billion (2022), creating white‑space for the GCC.

2. Where the Money Lands

| Sector | Gulf Flagship | Why It Matters |

|---|---|---|

| Renewables | AMEA Power – Aysha 1 Wind Farm, Ethiopia (US $620 m, 300 MW) | Powers 4 million homes; anchors Horn of Africa green grid. |

| Ports & Logistics | DP World – 30‑yr Dar es Salaam concession (≤ US $1 bn) | Eases copper‑belt exports; adds cold‑chain for agri‑trade. |

| Mining & Metals | IHC – 51 % of Mopani Copper Mines, Zambia | Shows Gulf appetite for tech‑enabled, brown‑field assets. |

| Agri‑Tech | Egypt AgTech Park (US $5.6 bn UAE project) | Delivers food security for both regions via climate‑smart farming. |

| Healthcare | UAE‑funded 60‑bed hospital, Juba | Tackles Africa’s US $25 bn health‑infrastructure shortfall. |

Investment velocity: GCC FDI stock in Sub Saharan Africa grew at 35 % CAGR (2010 23) [14], while the UAE has pledged an additional US $4.5 billion to mobilise 10 GW of clean power by 2030.

3. The Family Office Edge

- Speed over Sovereigns – Private mandates reach close in 4‑6 months versus multi‑year state timelines.

- Flexible Capital – Sukuk slices, SPVs, and blended‑finance stacks cover tickets from US $5‑200 million.

- Cultural Fit – Shared Sharia principles smooth deal structuring and local JV negotiations.

4. Risk Radar & Mitigation

| Headline Risk | Smart Mitigants |

|---|---|

| Political / Regulatory (High) | Minority positions with veto rights; MIGA & ICIEC wraps. |

| Currency (Medium) | Match local revenues to debt; World Bank PRG swaps. |

| Legal & Compliance (Medium) | UK‑style ESG diligence; arbitration in Kigali or ADGM. |

| Exit Liquidity (Medium) | Put options with DFIs; dual Africa‑GCC IPO routes. |

5. Action Playbook for Family Offices

Co Investment Archetypes

- Club Deals: Team with Africa50 or Afreximbank for US $100‑500 m infra rounds.

- Venture Syndicates: Allocate 5‑10 % of AUM to pan‑African VC funds for fintech and logistics upside.

Partnership Structures

- Local JVs: Target ≥ 30 % domestic stakes for political cover.

- Impact‑Linked Carry: Tie GP promote to SDG metrics—jobs, grid connections, emissions avoided.

Due‑Diligence Checklist

- Clear title to land or mineral rights

- Guaranteed grid access / sovereign offtake

- FX convertibility ≤ 30 days

- Capped contingent liabilities

Impact Metrics

Adopt IFC’s Operating Principles or GIIN IRIS+ to satisfy next‑gen heirs demanding purpose with profit.

6. Closing Signal

With US $100 billion already deployed and fresh pledges such as Saudi Arabia’s US $41 billion decade package , Gulf family offices are no longer side players—they sit at the intersection of Africa’s development gap and their own diversification drive. Those who blend rapid decision making with rigorous risk controls stand to earn desert capital, savannah returns.